CKICK TO ENLARGE

CKICK TO ENLARGE

THANKS to last-minute bargain hunting, the Malaysian stock market ended the final trading day of 2021 sharply higher, a reversal from the weakness seen in the previous session. However, it still made a loss for the entire year.

The equity market had largely traded in the negative territory throughout Friday amid subdued investor sentiment until the final hour of trading when buying momentum set in.

The benchmark FBM KLCI gained 23.92 points, or 1.55%, to finish at 1,567.53 points yesterday.

Turnover was at 2.52 billion shares valued at RM1.86bil.

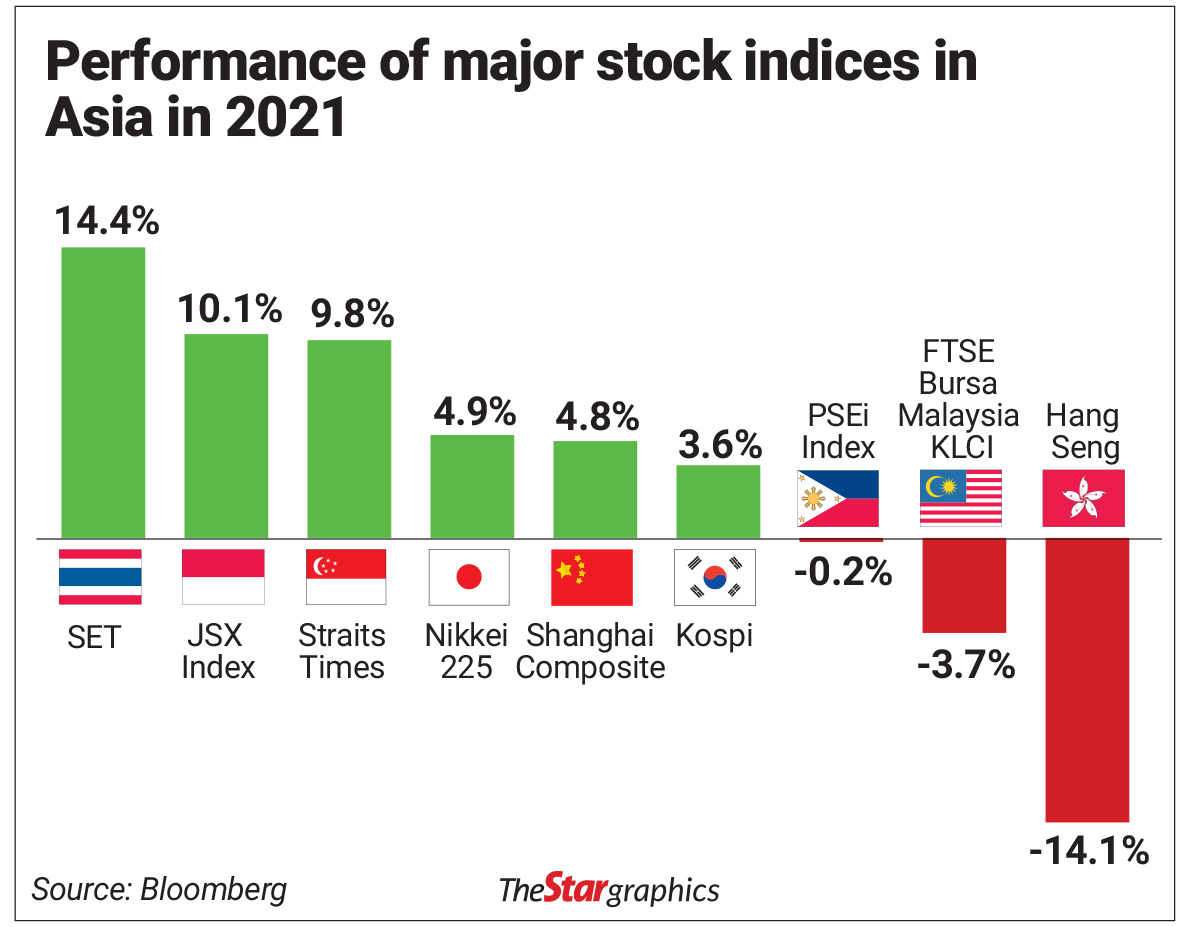

Overall, the Malaysian stock market is counted as the worst performer in Asean in 2021.

Having lost about 3.7% through 2021, the FBM KLCI was also the second worst-performing market in Asia, after Hong Kong.

The negative returns generated by the 30-stock index were due mainly to the decline in the share prices of glove, energy and palm oil companies.

In general, sentiment towards the Malaysian stock market was dampened due to a series of negative developments in 2021. These included the reimposition of lockdowns due to rising Covid-19 cases; political uncertainties that eventually resulted in the change of Prime Minister; forced labour allegations against certain manufacturers, including glove players; and announcement of higher taxes during the tabling of Budget 2022.

Volatile trend

In describing the FBM KLCI performance in 2021, Maybank Investment Bank Research (MaybankIB Research) said investors had instead been subject to a sisyphus-like string of disappointments and headwinds.

“Every time the market appeared to be on the cusp of gathering the requisite positive momentum to catch up with outperforming Asean peers, a new headwind has emerged, overshadowing the prima facie equity-favouring investment backdrop of rapidly-improving vaccine efficacy and availability, continuing accommodative fiscal and monetary policy, rebounding commodity prices, relative attraction versus fixed income given rising inflation and (United States) tapering concerns, as well as buoyant retail trading activity,” the brokerage explained.

The FBM KLCI reached its 2021-peak closing at 1,639.38 points on March 10.

It fell to its low of 1,480.92 points on Dec 14 on concerns over Budget 2022’s impact; and Omicron (a more contagious Covid-19 variant) impact on the reopening of the country’s economy and relaxation of travel restrictions.

MaybankIB Research noted the FBM KLCI spent much of the first half of 2021 range-bound as optimism around vaccine availability was offset by the slow pace of vaccinations and political tension before significant volatility set in through the second half of 2021 due to the imposition of the renewed national lockdown.

“The August change in Prime Minister coincided with the peak in pandemic restrictions, with a surge in vaccinations and paced economic reopening supporting the subsequent market uptrend,” MaybankIB Research said.

“However, a populist turn in policymaking into Budget 2022 (extended loan moratoriums, Cukai Makmur) deflated sentiment and overshadowed mitigating positives such as robust corporate reporting, undershooting non-performing loans and strength in the export-oriented manufacturing and commodities sectors,” it adds.

Sectoral performance

Of the 13 Bursa Malaysia sectorial indices, only four posted positive returns in 2021. The technology sector led the pack with a gain of 38%. This was followed by the industrial products and services sector, which posted a gain of 13%; the transportation and logistics sector, with a return of 8%; and the financial sector (1%).

Conversely, the main drags of the FBM KLCI were the healthcare (36%), energy (21%), construction (17%), utilities (12%) and plantation (10%) sectors in 2021.

The healthcare sector was the worst-performing sector due to the sharp correction in large glovemakers’ share prices, CGS-CIMB Research noted.

“The energy sector index fell due to concerns over weaker earnings, ESG (environmental, social and corporate governance) practices, low crude oil prices and cancellations of projects,” it said.

“The construction sector was impacted by slower progress billings, fewer new project wins and rising operating costs which would negatively impact earnings. Other concerns include political uncertainty which could cap the speed of recovery in the construction sector,” it added.

Despite crude palm oil prices rising to an all-time record high, the plantation sector also underperformed the FBM KLCI on ESG concerns, CGS-CIMB Research explained, pointing to allegations of forced labour in Sime Darby Plantations Bhd and FGV Holdings Bhd estates operations in Malaysia as well as labour shortage issues.

estates operations in Malaysia as well as labour shortage issues.

The utilities sector also face ESG risks.

It is also one of the sectors expected to be most affected by the one-off prosperity tax of 33% that would be levied on companies with chargeable income of more than RM100mil in 2022.

ESG concerns

Retail participation in the Malaysian stock exchange was high in 2021, with net buying totalling RM12.44bil as at Dec 24.

Local institutions and foreign investors, on the other hand, were net sellers in 2021 to the tune of RM9.27bil and RM3.17bil, respectively, as at Dec 24.

Analysts pointed to domestic political tensions and various ESG concerns affecting several companies in the glove, technology and plantation sectors as major reasons foreign investors sought to reduce their exposure to Malaysian equities.

MIDF Research noted that 2021 saw the impact of ESG concerns coming to the fore.

“The persistent ESG misconception in the plantation sector is well known and has seen this sector underperforming. There were other issues raised in the glove sector and lately, the technology sector became the latest sector to be hit,” the brokerage said.

“Nevertheless, we understand that there is a differentiating factor among the tech companies and its ESG adoption – we think companies with high ESG grading band rating will likely weather current issues as the fundamental remains intact,” it noted.